Small independent brewers left in limbo over Small Breweries’ Relief changes

- The UK’s small independent brewers have been left in limbo one year on from the Treasury’s announced changes to Small Breweries’ Relief (SBR).

- These changes could see more than 150 small brewers paying up to £44,000 extra per year to the Treasury. They could come into force within months leaving small brewers little time to prepare.

- New academic research shows that Treasury plans could weaken small brewers’ ability to compete with much larger breweries.

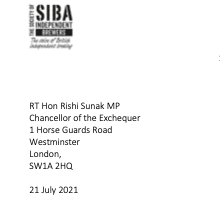

- The Society of Independent Brewers (SIBA) has today written to the Chancellor seeking urgent clarification to address the uncertainty faced by small businesses.

Letter to Chancellor Rishi Sunak from SIBA (Click to view)

One year ago today (21 July 2020) the Treasury announced changes to Small Breweries’ Relief (SBR) – a scheme under which small brewers pay a proportionate amount of beer duty compared to the Global companies that dominate the sector.

Twelve months later and small brewers are living under a cloud of uncertainty, unsure what the final changes will be or when they will be introduced. Today the Society of Independent Brewers (SIBA) has written to the Chancellor seeking urgent clarification.

“Small Breweries’ Relief is pivotal for brewers’ survival, and we have now faced a year of uncertainty not knowing when changes will be made or how much extra brewers will have to pay.” said Chief Executive of SIBA James Calder. “This is at a time when pubs have been closed for most of the past 16 months and small brewers are struggling to survive and repay debt. We therefore urge the Chancellor to support the sector and provide the certainty we need by not reducing SBR for those below 5,000hl.”

New research shows Government plans could weaken small breweries’ ability to compete

This comes as new academic research shows that Treasury plans to reduce duty relief support could weaken small breweries’ ability to compete against much larger brewers. Professors Geoff Pugh and David Tyrrall argue that the Treasury should consider improving duty relief for those in the middle instead of withdrawing or reducing it for smaller breweries.

Currently the UK’s smallest breweries pay 50% of the duty if they produce less than 5,000 hectolitres (hl) per annum, which is the equivalent of 900,000 pints or enough beer to fully stock 15 pubs for a year. Under new Treasury proposals, this 50% threshold will be reduced to 2,100hl, meaning that around 150 small breweries will have to contribute more in taxation to the Government.

Analysis by two economists, who have previously written extensively on SBR, shows these changes could weaken brewers’ competitiveness against the breweries further up the scale, especially those up to ten times as large, above 20,000hl. Instead, Professors Pugh and Tyrrall argue: “If there is a wish to remove an anomaly in the current structure, one way to do this would be to improve the duty relief for the 5001- 10,000hl category, rather than withdraw or reduce it for the 2,501-5,000hl category.”

Breweries have been left in limbo by treasury delays

The Treasury has been reviewing SBR since 2018 and by narrowly focusing on production costs and excise duty have argued that this gives an advantage to breweries below 5,000hl. If there was an advantage to producing at this level, it might be expected that there would be a bulge in the number of breweries between 2,501-5,000hl. However, as the research shows there is limited evidence for any effect of this on the distribution of small breweries.

As the new research demonstrates, the Treasury review did not consider the impact of market structure on small breweries of different sizes, particularly that as they grow in size they become more reliant on wholesalers to sell their products outside the local area and have to accept relatively lower margins. To take account of this Professor Pugh and Tyrrall considered the impact of Market Access Cost, which reflects the reduced selling price that small brewers receive as they grow and become more reliant on wholesalers. They infer that breweries producing between 2,501-5,000hl become substantially more dependent on wholesale sales but are only a little less squeezed on price than the smallest brewers.

Drawing on data from small breweries compiled by SIBA, Professors Pugh and Tyrrall show that once Market Access Cost is taken into account, breweries in the 2,501-5,000hl category may have a slight cost advantage in relation to breweries just above the 5,000hl level but this enables them to compete with the larger breweries.

This suggests that the issue is not that those in the 2,501-5,000hl category are over-compensated by beer duty relief for their costs disadvantages nor that they should have some or all of the relief withdrawn. Instead, it suggests that those in the 5,001-10,000 hl category are under-compensated by beer duty relief for their cost disadvantages compared to larger competitors.

Professors Pugh and Tyrrall conclude that SBR should continue to have the aim of enabling and encouraging the development at the lower end of the sector and it would seem to be a mistake to penalise those between 2,501-5,000hl.

Professor Geoff Pugh said: “Since 2002, Small Breweries’ Relief has supported a thriving craft sector of the brewing industry by reducing excise duty to offset the effects of small scale and low sales prices.

“The evidence suggests that the cost to the taxpayer is compensated by encouraging entrepreneurship and innovation and therefore more varied choice for consumers, job creation, and competition in an otherwise increasingly concentrated industry. The proposals for reform therefore require overwhelming evidence that the claimed benefits do not come at the expense of these actual benefits.”

The letter to the Chancellor can be found here – Letter to Chancellor Rishi Sunak from small brewers (PDF)